What is a blockchain? What has it got to do with cryptocurrency? Where do these terms and technologies all fit into the ever-expanding web3 ecosystem? And what can blockchain technology do for individuals and businesses? This basic beginner’s guide to blockchain covers everything you need to know.

What is a blockchain?

A blockchain is a distributed database system, or ledger, that enables an online list of transactions. Distributed ledger technology is another name for blockchain technology. A ledger is like a special notebook that keeps track of all the transactions and balance changes occurring in a specific system or network. In this case, the ledger stores information about cryptocurrency (digital money).

This ensures that a blockchain is immutable; everyone has the same information, and nothing changes without everyone knowing.

With blockchains, users can send and receive peer-to-peer (P2P) transactions globally without the need for intermediaries (e.g., banks).

In short, cryptocurrency is digital money, and a blockchain is the ledger for that cryptocurrency. A blockchain is a distributed database that allows users to send, receive, and store their cryptocurrency by themselves and without needing a bank.

How does it work?

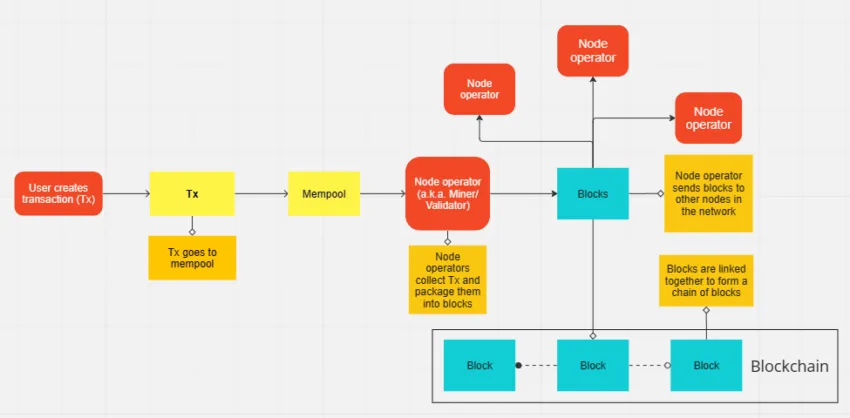

The blockchain keeps a permanent record of every transaction and user account ever created on the blockchain. When users create transactions, they don’t immediately go to their recipients. They wait in a transaction queue called the mempool.

Special workers called miners, or validators collect these transactions from the mempool and put them into data packages called blocks. To go into more detail, miners and validators are able to accept and process transactions and create blocks because they run nodes. Therefore, the names miners and validators are interchangeable with node operators.

A node is an individual component within a larger system or network. In the context of computer science, a node is simply a device or computer connected to a network (i.e., a group of nodes creates a network). Therefore, node operators (i.e., miners and validators) operate computers called nodes that house the software for maintaining the blockchain.

To continue, these special workers send the blocks to other node operators within the network. Node operators receive blocks to verify if they are formatted properly. If they are formatted properly, the node operators accept them into their record of the blockchain.

In other words, the block is appended or linked to the previously accepted block, forming a chain of blocks called a blockchain. The blockchain is simply a record of a chain of blocks (or transaction data) replicated across computers all over the world. After this entire process, the transaction is complete.

The blockchain doesn’t actually send coins or tokens. The balance is debited from one user and credited to another. Furthermore, this process typically occurs within a matter of minutes or seconds, depending on the blockchain.

Once the information is written or the block is added, it cannot be changed without the agreement of the nodes running on that network. Each block has a timestamp and link to the previous block. Anyone can read this list of transactions.

Why is blockchain important to cryptocurrency?

Blockchains were first created in 2008 and then implemented in 2009 by Satoshi Nakamoto, the anonymous creator of bitcoin.

Blockchains create cryptocurrencies, similar to how the U.S. Treasury mints dollars and coins. To be clear, you can have a blockchain that does not issue any cryptocurrency. They are — for all intents and purposes — two separate things.

Using digital money has certain risks if not implemented properly. Firstly, if you can create money digitally, what stops someone from counterfeiting it? Secondly, what happens if the database holding all of the transaction records and account balances goes down?

Lastly, who will maintain the database, and if they maintain it, what stops them from taking advantage of it? To put it simply, blockchains solve some of the problems associated with digital forms of money. When you create a transaction with a cryptocurrency, the blockchain stores it in blocks. The reason that the blocks are linked together sequentially, cryptographically, and distributed to nodes across the world is to:

- Prevent double spending (a problem with digital currencies)

- Preserve privacy, and secure the transaction data

- If any one or multiple computers (nodes) go down, a record of the blockchain still exists

- Anyone can run a node to secure the network

Blockchains are decentralized, immutable, and censorship-resistant. As a result, they are popular for recording transaction data. As opposed to centralized ledgers or bookkeeping, wherein records can be altered, blockchains can not. Cryptocurrencies not only need a way to record transactions but also need a way to issue tokens and coins. This is where blockchains come in.

What problems can blockchain technology solve?

- Eliminates the “middleman” — or need for a mediator, which a bank usually represents. Even online payment methods such as PayPal require an integration with a bank account to work. Yet blockchain technology means we can confirm transactions, confirm identities, and verify contracts, all without the need for a third party.

- Trust issues — The network builds trust for us through a combination of complex math problems that must be solved, proven, and then verified by the rest of the network before any new piece of information is added. Compare this to making a payment online; several elements need to be individually trusted, for example, banks, websites, and payment systems.

- Transparency — In public blockchains, all transactions are available for viewing; this enables a level of integrity and accountability that has not existed in previous financial systems.

- Control — Blockchain is a decentralized system, no individual can control what happens, and things can only change via consensus.

- Decentralization — Blockchains became famous for their ability to securely decentralize the issuance of currency. The problem with centralized currency issuance is that the issuer can arbitrarily print more currency units, which causes its value to plummet. This is known as inflation.

- Censorship resistance — Because anyone can maintain the record of transactions (i.e., blockchain), no one can be denied access to the ledger. This is particularly useful for P2P transactions, where peers want to confirm that the counterparty has the ability to pay.

- Immutability — Records stored on the blockchain are permanent. In traditional finance, centralized entities have the ability to alter or “cook their books,” to defraud customers. With blockchain technology, this is nearly impossible.

Blockchains as P2P payment systems

By now, we know that a blockchain stores information about financial value. This records transfers between entities and gets rid of the need for a centralized third party like a bank. And as we know from the multiple banking crises that have affected the financial order of late — including the recent collapse of crypto-friendly banks in the U.S. — the current banking system is a tainted and complex web with a number of weaknesses in tow.

For example, although you immediately complete a transaction when you pay for goods and services, it usually doesn’t settle until days later. This means that the cash isn’t actually sent or transferred until later. If you are sending money, the bank automatically credits the recipient.

That is because your bank has to “send” money to another bank (in reality, they are resolving ledgers with each other). If your bank does not have a relationship with the vendor’s bank, or the banks are in different countries, using different currencies, the process will take even longer.

All the while, you are incurring fees for sending or accepting payments because you have to pay the middlemen (intermediaries). However, with a blockchain, you can simply send payments between people (P2P) without intermediaries.

Note that while bitcoin was originally hailed as the transformative P2P digital currency, as web3 has expanded, other digital currencies make more sense for P2P value transfer. Bitcoin Cash (BCH) is one such example; the currency was launched to improve the scalability and speed issues lingering within the Bitcoin ecosystem. BCH works as a means of remittance and e-commerce settlement and can even handle micropayments.

Ways to apply blockchain technology

The potential of blockchain technology to transform multiple industries is yet to be realized. The applications are vast across many sectors. Here are just some ways that blockchains improve several industries:

- Smart contracts: In addition to storing a unit of value, some blockchains can be used to store different types of digital information or state. This means code can be programmed to trigger automatically when conditions are met from external data feeds (e.g., stock prices, energy usage).

- Internet of Things: This term describes the growing number of everyday objects that can connect to a more extensive network via the internet. Blockchain technology offers the opportunity for further scalability and integration.

- Fundraising: The charity industry can benefit from the transparency offered by blockchain transactions. Often charities can face challenges ensuring that the public has trust in the funds arriving at their intended destination. Blockchain means that information on the allocation of funds is visible to funders.

- Healthcare: Because blockchain technology is so secure and reliable, it’s the perfect method of recording and storing sensitive information such as healthcare data.

- Supply chain management: The ability to precisely track processes with complete transparency is useful from both the production and consumer point of view. Customers can know the exact origin and contents of their products, helping to reduce scandal and maintain integrity for companies.

What’s next for blockchain?

As more and more companies are utilizing blockchain technology to create greater reliability and transparency across digital platforms, solving problems in everything from supply chains to healthcare records, the potential of this technology to transform society is ever more apparent. For now, adoption, awareness, and affordable solutions to integrate blockchain into web2 processes are all key in swapping legacy systems with decentralized web3 solutions.

Frequently asked questions

What is the difference between blockchains and cryptocurrency?

Why are blockchains popular?

Why are blockchains decentralized?

How are blockchains censorship resistant?

Trusted

Disclaimer

In line with the Trust Project guidelines, the educational content on this website is offered in good faith and for general information purposes only. BeInCrypto prioritizes providing high-quality information, taking the time to research and create informative content for readers. While partners may reward the company with commissions for placements in articles, these commissions do not influence the unbiased, honest, and helpful content creation process. Any action taken by the reader based on this information is strictly at their own risk. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.